A2B’s Audit Risk assessment and planning

Executive Summary

The report is about the A2B’s Audit Risk assessment and planning. A2B Australia is an Australian owned company that was listed on the Australian Stock Exchange in December 1999 and is an ASX 200. Reg Kermode founded the Firm. In 1976, the firm set up Cabcharge, an invoice payment scheme to offer a way for non-cash means to pay taxi fares and is still the sole operator of the in-taxi service. The other main operations of A2B are Mti and 13 cabs. In this report, the areas have been identified where there is significant doubt on the Going Concern of the A2B like Decrease in cash flow, Increase in Liability, and lower Total debt to equity ratio. Moreover, the accounts have been identifying where there are material misstatements like Valuation of Taxi plate license and goodwill. The other material misstatement is the wrong classification of Loans and borrowings. Furthermore, planning materiality has been set out along with its base in Revenue and trade and other receivables of the company. Finally, the report tells about the factors which can affect the 2020 audit plan due to the acquisition of Gold Coast Cabs.

A2B’s Operations

The operations which the A2B Australia conducts are (A2B Australia Limited Annual Report , 2019):

- 13 cabs: It is the Taxi network which A2B operates in whole Australia. It had vehicle fleet over 10000. It is firmly established in big cities of Australia like Melbourne, Sydney, Brisbane and Adelaide. It provides 24/7 booking services through three Australian-based contract centers.

- Mti: It is basically the service of software development. Mti develops the advanced and innovative saaS dispatch and booking service platforms.

- Cabcharge: It is the account payment system which was established in 1976 in order to facilitate the taxi passengers to pay for the fare. This system is the alternative of cash payment system.

A2B’s Going Concern

It is the responsibility of an auditor not only audits the financial statement of the company but also relates the management use of Going Concern’s principle in the preparation of the financial statement. ISA 570 is the international standard of Auditing which relates to the Going Concern principle (INTERNATIONAL STANDARD ON AUDITING 570 (REVISED)GOING CONCERN, 2016). The areas which may significantly doubt on the A2B’s ability to continue as a going concern are:

- Decrease in cash and cash equivalent from 22,253(FY18) to 19,172(FY19). The reason for this decline is the reduction in net cash flow in operations in FY19 as compare to that of FY18. Company receives less amount from its credit customers in FY19. However, there is no negative cash flow in operating cash flow which is the biggest factor in considering significant doubt on company’s Going Concern principle.

- Increase in contract, trade and other payable to 37,913 from 32,940 (FY18). The reason for this increase is the contract liabilities company have of 9091 in fiscal year 2019. And in 2018 there were no contract liabilities.

- The provision of employee’s wages and salaries have been increased this year due to increase in wages in future.

- Increase in Impairment loss on trade receivables arising from contracts with customers to 1360 from previous year which was 466.

- The company’s total debt to equity ratio is 12.77% which means company relies on equity financing so investor will expect more profit on investment so future dividends might increase. Equity investment is risky as there might be chance where company’s actual owners can lose their control in future (Advantages vs. Disadvantages of Equity Financing, n.a).

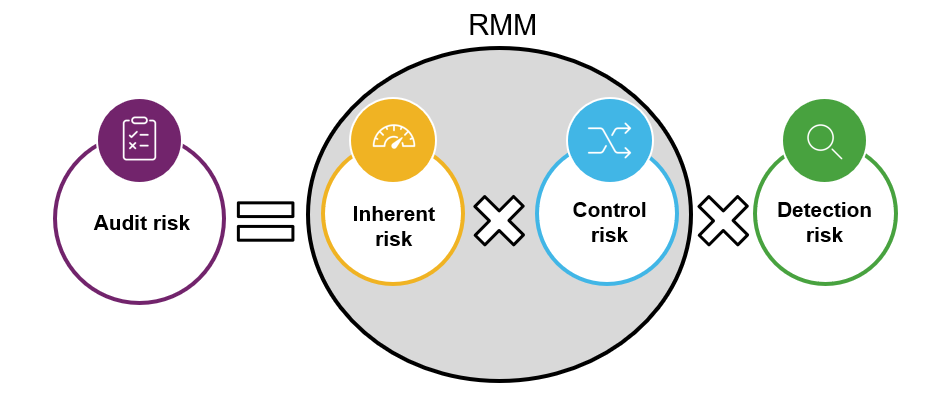

A2B’s Material Misstatement and its Key Assertion

As an auditor one should assess the risk of material misstatement of an organization’s financial statement because the financial statement must have been misstated to a material degree (Bragg, 2020). There are some areas in financial statement of A2B where the material misstatement exists along with their key assertion at risks (A2B Australia Limited Annual Report , 2019). These are:

- Valuation of Taxi plate license ($17.5m FY19): The external auditor of A2B, who is KPMG, stated in the audit report that this is the key audit matter. Firstly, the level of discretion the auditor needs in assessing the forecasts for projected sales determined by management is an important factor in the use model’s taxi plate license value. Secondly, changes in customer preferences and regulatory legislation continue to challenge the pace of sales growth for the taxi companies. This create uncertainty in the assumption of valuation of Taxi plate License. “Valuation” is the key assertion at risk used to identify the material misstatement. Because as an auditor one has to consider inaccurate forecasted values of the possible outcomes.

- Valuation of the Goodwill ($25.7m FY19): The external auditor of A2B, who is KPMG, stated in the audit report that this is the key audit matter. A2B Australia operates in that environment where the industry is impacted by disruptive technologies. Additionally, there are changes in local legislation concerning taxi service rates that can be enforced as payments are made. This factor may cause the goodwill of the company being impaired. And there is no impairment loss of Goodwill in the financial statement of A2B from which goodwill might be considered overstated. Moreover, the discount rate used in valuation in goodwill are complicated in nature. The assertion level of this risk is inherent risk as there is susceptibility of an assertion of whether the goodwill value is misstated. “Valuation” is the key assertion at risk for this material misstatement.

- Omission or wrong classification of loans and borrowings: Although company is more of an equity financed company, but the company have minimum loans and borrowings from which an auditor might conclude that there had been omission or undervaluation of loans and borrowings of the company. Moreover, loans and borrowings are the part of current liabilities so wrong classification of this account. Generally, loans and borrowings are part of Non-current liability. “Classification of liability” is the key assertion at risk of this material misstatement.

Planning Materiality and its base

Planning materiality generally refers to the amount of misstatement set by the auditors at the planning stage of an audit depending on the financial report materiality. The auditor ‘s planning materiality used to determine whether the error as entity or composite was significantly misstated in the financial statements. And those misrepresentations may lead users who use the financial details to make the wrong decision (Kong, n.a). The materiality base and set planning materiality of some items in financial statement of A2B are:

- Revenue (3%-6%): Less than 3% it is immaterial and greater than 6% is the material. The reason for this base is that the A2B company is exposed to some credit risk when it receives taxi service fee income.

- Trade and other receivables (5%-10%): Less than 5% it is immaterial and greater than 10% is the material. The reason for this base and percentage is because there are expected credit loss which caused the impairment of trade and other receivables.

Gold Coast Cabs Acquisition

Lately A2B acquired Gold Coast Cabs (fleet of approximately 400 taxis) to further advances its strategy of offering quality services on a national basis. This acquisition will definitely affect the 2020 audit plan of the A2B Australia in the following ways:

- The acquisition will increase the scope of the audit because the auditor will further obtain sufficient evidence in the event of acquisition. The audit of an acquisition takes time than usual.

- The auditors might be changed because auditor with the knowledge of business combinations under IFRS rules will be hired.

- the additional documents will be audited by the auditors like the due diligence workpapers or any other legal documents (CONDUCTING AN EFFECTIVE POST-MERGER & ACQUISITION AUDIT, 2019).

- The audit team might have the additional responsibility to interview key members of the A2B like accounting personnel or CFO.

Conclusion

A2B Australia limited is one of the biggest land transport company in Australia. And it had several business units which are Cabchage (Online Payment system), 13 Cab (Taxi Network), and other cloud services. So, its audit process is quite the complicated one where there are a lot of items in Financial statement which requires valuation such as trade and other receivables, taxi plate services or goodwill so these are key audit matters for an auditor. The auditor can also suspect material misstatements on these items or accounts. Furthermore, the objectives and scope of a 2020 audit will change due to the acquisition of Gold Coasts Cabs.

References

(2019). A2B Australia Limited Annual Report . A2B Australia.

Bragg, S. (2020, January 02). Accounting Tools. Retrieved from Accounting Tools website: https://www.accountingtools.com/articles/2017/5/13/risk-of-material-misstatement

Business owner’s playbook. (n.a). Retrieved from Business owner’s playbook website: https://www.thehartford.com/business-insurance/strategy/business-financing/equity-financing

(2016). INTERNATIONAL STANDARD ON AUDITING 570 (REVISED)GOING CONCERN. INTERNATIONAL STANDARD ON AUDITING.

Kong, S. (n.a). Wiki Accounting. Retrieved from Wiki Accounting website: https://www.wikiaccounting.com/planning-materiality/

KPM CPAs and Advisors. (2019, December 21). Retrieved from KPM CPAs and Advisors website: https://www.kpmcpa.com/conducting-an-effective-post-merger-acquisition-audit/

Hire Expert Writers at Affordable Price

WhatsApp

Get Assignment Help