MarketLine Industry Profile Report

Mobile Phones in Australia May 2019

EXECUTIVE SUMMARY

Market value

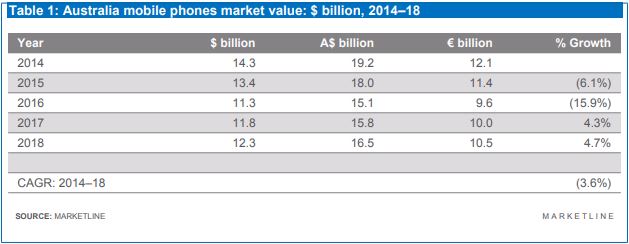

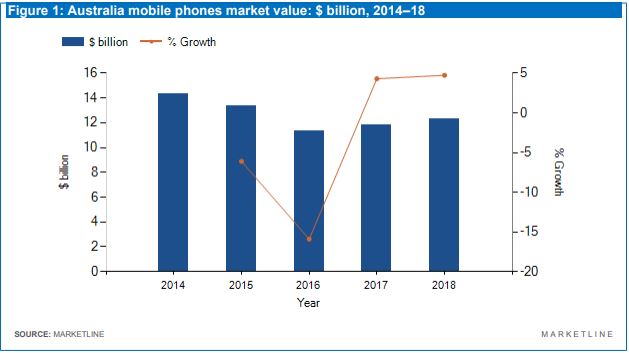

The Australian mobile phones market grew by 4.7% in 2018 to reach a value of $12.3 billion.

Market value forecast

In 2023, the Australian mobile phones market is forecast to have a value of $13.3 billion, an increase of 8.1% since 2018.

Market volume

The Australian mobile phones market shrank by 2.5% in 2018 to reach a volume of 376.4 Average MOU.

Market volume forecast

In 2023, the Australian mobile phones market is forecast to have a volume of 309.6 Average MOU, a decrease of 17.7% since 2018.

Geography segmentation

Australia accounts for 3.6% of the Asia-Pacific mobile phones market value.

Market rivalry

The Australian mobile phones market is dominated by a small number of large-sized companies, such as Apple, Samsung, TCL and Sony. Rivalry is increased due to the limited number of competitors and the high penetration of mobile phone devices, which intensifies R&D expenses and price competition.

MARKET OVERVIEW

Market definition

The Mobile Phones market includes mobile phone service revenues and average minutes of use (MOU). Market values are made up of total mobile revenues containing revenues from mobile service providers and other members of the mobile service value-chain for the provision of mobile telephony services, excluding revenues from the sale of devices. Market volumes are made up of two segments: prepaid and postpaid, which consist of prepaid average monthly MOU and postpaid average monthly MOU. Minutes of use are made up from the average of voice minutes used in mobile subscriptions, including both incoming and outgoing calls, but not including M2M/IoT voice services. All currency conversions are carried out at constant average annual 2018 exchange rates. For the purposes of this report, the global market consists of North America, South America, Europe, Asia-Pacific, Middle East, South Africa and Nigeria. North America consists of Canada, Mexico, and the United States. South America comprises Argentina, Brazil, Chile, Colombia, and Peru. Europe comprises Austria, Belgium, the Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Netherlands, Norway, Poland, Portugal, Russia, Spain, Sweden, Switzerland, Turkey, and the United Kingdom. Scandinavia comprises Denmark, Finland, Norway, and Sweden. Asia-Pacific comprises Australia, China, Hong Kong, India, Indonesia, Kazakhstan, Japan, Malaysia, New Zealand, Pakistan, Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam. Middle East comprises Egypt, Israel, Saudi Arabia, and United Arab Emirates.

Market analysis

The Australian mobile phones market experienced volatile growth during the historic period with growth fluctuating between -16% and 4.7%. The forecast period is expected to be more stable with growth in the market fluctuating between 1% and 2.3%. The mobile phones market has begun to saturate as more and more consumers already possess a mobile phone of some kind. As a consequence, activity in the market is reduced as most buyers will not need to purchase new smartphones on a regular basis. This has impacted volume growth in the market and resulted in its deceleration. Competition in the market is fierce as mobile phone manufacturers try to differentiate their products from the competition in order to increase their market share. The Australian mobile phones market had total revenues of $12.3bn in 2018, representing a compound annual rate of change (CARC) of -3.6% between 2014 and 2018. In comparison, the Japanese and Chinese markets grew with compound annual growth rates (CAGRs) of 0.5% and 3.5% respectively, over the same period, to reach respective values of $66.7bn and $159.0bn in 2018. Market consumption volume increased with a CAGR of 1.2% between 2014 and 2018, to reach a total of 376.4 average MOU in 2018. The market’s volume is expected to fall to 309.6 average MOU by the end of 2023, representing a CARC of -3.8% for the 2018-2023 period.

The increase in online retailers selling the same kind of mobile phones at cheaper prices reduced the number of consumers purchasing mobile phones from high street stores to a great extent. In addition, consumers tend to buy second-hand or used mobile phones from online retailers as a cheap alternative, while other consumers tend to keep their mobile phones for more than five years due to them not being that different from the newest models, decreasing market growth overall. On the other hand, copies of popular mobile phones, which have to some extent the same characteristics as the originals, can be found online for very cheap prices. These imitations are used by consumers who cannot afford the originals but want to project a high social stature. Due to the fact that popular mobile phones such as the iPhone XR or Samsung Galaxy S10+ are being used as social stature indicators because of their expensive prices, consumers who do not have the economic power to purchase those kinds of mobile phones, but want to demonstrate a certain level of social stature, will purchase cheap imitations of them, which undermines market growth. Postpaid had the highest volume in the Australian mobile phones market in 2018, with a total of 282.6 average MOU, equivalent to 75.1% of the market’s overall volume. In comparison, prepaid had a volume of 93.8 average MOU in 2018, equating to 24.9% of the market total. Postpaid was the most successful segment for the mobile phone market due to it seeming to be the “cheaper” option according to consumers. Postpaid phones require consumers to sign a contract with a mobile network operator making them pay a monthly sum for their mobile phones, usually up to 12 months. The monthly sum varies according to the mobile network operator and is at least 500% cheaper than the total cost of the phone. Because most consumers are willing to pay a smaller price for a longer period of time for a product, rather than a larger price for a shorter period of time, it makes them feel more secure and that they got a “cheaper” deal. Prepaid was the least successful segment as it creates the opposite feeling to postpaid mobile phones, even though prepaid mobile phones are a great deal cheaper than postpaid ones. The performance of the market is forecast to accelerate, with an anticipated CAGR of 1.5% for the five-year period 2018 – 2023, which is expected to drive the market to a value of $13.3bn by the end of 2023. Comparatively, the Japanese market will increase with a CAGR of 2.6%, and the Chinese market will decline with a CARC of -0.6%, over the same period, to reach respective values of $75.7bn and $154.5bn in 2023. The mobile phones market is expected to grow during the forecast period. The market is positively correlated with technology; as technological advantages occur, the mobile phone market’s growth will increase. At the moment, Samsung, Huawei and Oppo have launched a series of new foldable smartphones, which is a ground breaker for the market, increasing growth in the long-run. However, as more mobile phone manufactures produce highly technological products, competition will rise, decreasing the market’s growth overall. Consumers who purchase new mobile phones now will cause saturation in the market, as consumers are resistant to purchasing a new phone until there is a new technological advancement. Instead, they will turn to cheaper alternatives such as second-hand mobile phones, mobile phones imitations, or they will keep their mobile phones for a longer period of time. When the new technological advancement occurs, growth will rise again. The market is doomed to operate in a vicious circle, highly influenced by consumers’ behavior and technological advantages.

MARKET DATA

Market value

The Australian mobile phones market grew by 4.7% in 2018 to reach a value of $12.3 billion. The compound annual rate of change of the market in the period 2014–18 was -3.6%.